India’s digital currency, known as the Digital Rupee or e-Rupee, made its debut in the last quarter of 2022 within the country’s financial sector. The Reserve Bank of India (RBI) is responsible for issuing this central bank digital currency (CBDC). On December 1, 2022, the RBI introduced the e-Rupee pilot program, initially limited to selected user groups in specific cities.

Currently, in early July 2023, participation in the pilot program is by invitation only, requiring a special invitation from your bank to join. During the past six months, the RBI has been gradually expanding the availability of the e-Rupee, extending invitations to more cities and bank customers. Once you receive your invitation, you’ll likely be eager to explore and utilize this new Indian CBDC.

That’s where this guide comes in handy. It aims to equip you with a comprehensive understanding of acquiring and using the digital rupee, ensuring you’re fully prepared to maximize its benefits.

Digital Rupee: A Primer for Beginners

Step 1: Obtain an Invitation

The digital rupees are accessible only through a pilot program that operates on an invite-only basis. Initially launched by the Reserve Bank of India in Mumbai, Bengaluru, New Delhi, and Bhubaneswar, the program involved a select group of banks such as the State Bank of India, ICICI Bank, Yes Bank, and IDFC First Bank.

However, the RBI swiftly expanded the pilot program to include other locations as well. Additionally, the list of participating banks expanded to include Union Bank of India, Kotak Mahindra Bank, HDFC Bank, and Bank of Baroda. The program continues to grow, with five more banks, including Axis Bank, Canara Bank, IndusInd Bank, Punjab National Bank, and Federal Bank, joining in mid-2023.

Unfortunately, there is no way to ensure immediate receipt of an invitation from your bank. When your name comes up on the list for the Closed User Group (CUG), your bank will reach out to you. You will receive an SMS and an email inviting you to participate in the e-rupee pilot program. Therefore, it is important to monitor your inbox and phone notifications.

Step 2: Get the digital rupee app by following these steps

After receiving your invitation, proceed to download the digital rupee app. Simply search for “Digital Rupee app” on the Google Play Store or Apple App Store.

You may notice that various banks have their own apps, each with a slightly different user interface and color scheme. However, do not be misled by these surface-level dissimilarities. Despite the individual e-Rupee apps for each bank participating in the RBI’s CBDC pilot, the backend of all these apps remains consistently provided by the RBI. This approach ensures a standardized user experience, irrespective of the bank associated with the app.

Step 3: Registration Process

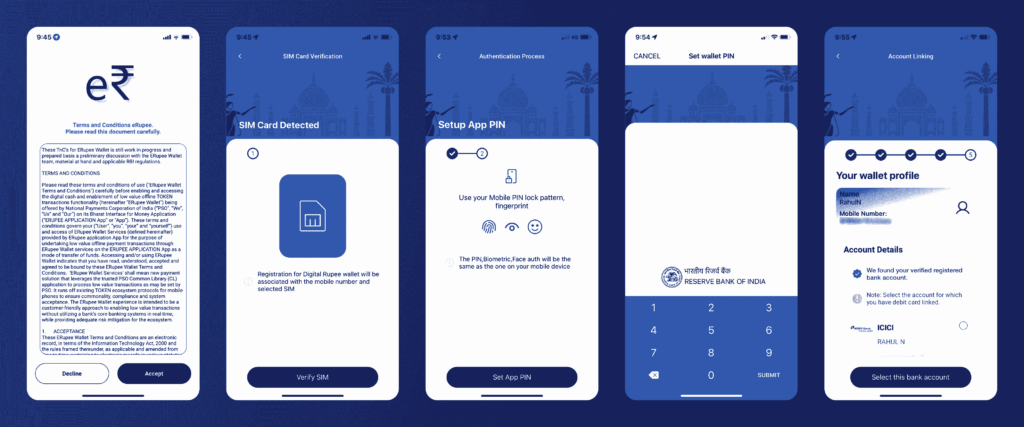

Upon launching your bank’s e-Rupee app for the first time, you will be prompted to grant certain permissions such as access to your contacts and text messages. Following that, you will need to agree to the app’s terms and conditions. Simply scroll down to the bottom, tap ‘Accept,’ and you will receive a brief overview of the e-Rupee.

Now, it’s time to proceed with the registration process. The app will request confirmation of the SIM card associated with your bank account. After completing the SIM verification, you will be prompted to set up a personal identification number (PIN) for the app. This PIN can be your device PIN, lock pattern, or even biometric credentials such as fingerprints. It enables you to access the app without requiring an OTP each time.

Next, you will need to enter your name and follow the on-screen instructions. When you reach the ‘Set Wallet PIN’ page, choose a unique PIN specifically for your digital wallet, distinct from the app PIN. The subsequent step involves linking your bank account to the e-Rupee app. The app will automatically detect the account associated with your mobile number.

Lastly, to complete the Know Your Customer (KYC) verification process, you may be asked to provide details of your debit card, including the last six digits and the expiry date. And there you have it! You have successfully completed the registration process. So, obtain your invitation, download your bank’s e-Rupee app, complete the registration, and you are now ready to experience the Indian CBDC.

Mastering the Digital Rupee

As a participant in the e₹ pilot program, you have the opportunity to utilize the digital rupee for both person-to-merchant (P2M) and person-to-person (P2P) transactions. This means that you can make payments for goods and services at various retail outlets, shopping malls, and other businesses that exhibit a QR code specifically for digital rupee transactions. Just ensure that the retailer you are patronizing possesses a digital rupee account.

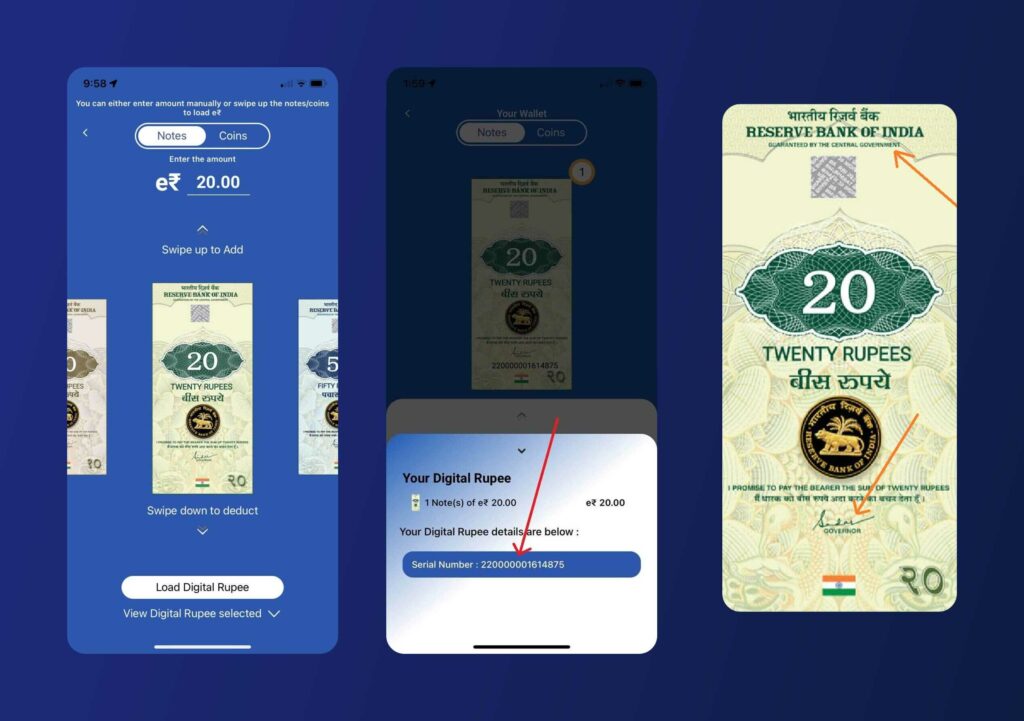

Furthermore, you have the capability to transfer funds between accounts, essentially using e₹ in a similar manner to physical cash. The digital rupee corresponds to the denominations of its physical counterpart. You will come across digital tokens in denominations ranging from e₹0.50 to e₹2,000, including e₹1, e₹2, e₹5, e₹10, e₹20, e₹50, e₹100, e₹200, and e₹500.

Each digital rupee token is assigned a unique serial number, which functions as its digital identifier. This distinct serial number enables the tracking of the individual token on the blockchain, enhancing security and providing a traceable path for every token. Moreover, as a form of legal tender, e-rupee tokens bear the name and logo of the Reserve Bank of India (RBI), along with the signature of the RBI Governor, similar to physical rupee notes.

Apart from that, to add funds to your digital rupee wallet, there are two methods: receiving funds from another user or transferring funds from your bank account. The procedure for loading your digital rupee wallet is similar to topping up a prepaid or UPI wallet. You have the option to utilize your debit card or any UPI app such as GPay or Amazon Pay.

Effortlessly Send and Receive Rupees Online!

Digital rupee transactions function similarly to regular cash transactions but in a digital form. For instance, if you wish to send e₹700 to a friend, you have various options. You can send one e₹500 token along with one e₹200 token, or you could choose to send seven e₹100 tokens, or even three e₹200 tokens and one e₹100 token, or perhaps 700 e₹1 tokens. The decision is yours.

However, what happens if you need to send an amount that doesn’t fit precisely into these denominations, such as e₹10.79 or e₹10.09? The Reserve Bank of India (RBI) has taken this into consideration. In such cases, the system will round off the amount to the nearest available denomination. For example, if you’re sending e₹10.79, it will be rounded up to e₹11.00, and if you’re sending e₹10.09, it will be rounded down to e₹10.00.

You have the option to send and receive money using either a QR code or a phone number. However, at present, you can only carry out transactions with other participants enrolled in the pilot program.

How to Convert Digital Rupees Back into Hard Cash

Certainly, it is possible to exchange your e-Rupees for physical currency. The reason behind this is that the digital rupee holds the same legal value as its physical counterpart, serving as an electronic representation of the rupee we commonly utilize. Once the digital rupee is implemented nationwide, you will have the option to approach any nearby bank and convert your digital rupee into physical cash.

Furthermore, at any time you desire, you have the ability to redeem a portion or the entirety of the funds stored in your e-Rupee wallet. The amount you redeem will be promptly transferred to your associated bank account.

What is the Functioning of the Digital Rupee?

The e₹, also known as the digital rupee, is a digital form of India’s official currency, reflecting the same denominations as physical cash that is currently in circulation. These digital tokens, which are authorized by the RBI, represent the currency we use in our daily lives.

Instead of delving into the intricate technical details, the RBI distributes these tokens through Token Service Providers (TSPs), who then pass them on to end users. Banks participating in the e₹ pilot program will obtain these tokens from the RBI through TSP merchants.

By issuing e₹ online, the RBI avoids the operational expenses associated with physical cash, such as printing, storing, and transporting. To store and utilize e₹, you will require a digital wallet, which is essentially a mobile application that serves as the digital rupee app. This wallet securely stores your e₹, enabling you to perform financial transactions electronically.

Conclusion

The digital rupee in India aims for an inclusive and efficient financial system. RBI is making efforts for a user-friendly and secure ecosystem. It offers faster transactions, global transfers, and 24/7 availability, surpassing traditional banking. The e-Rupee reduces costs and eliminates physical manufacturing. It streamlines government payouts, improving efficiency in subsidies, tax refunds, and scholarships.

The success of the digital rupee depends on accessibility and user-friendliness. It should be easy to navigate on smartphones for all, including those excluded from traditional banking. As the pilot program expands, more people can experience the benefits of this new currency.

To know more about Digital Rupee, go check out SunCrypto Academy.

Disclaimer: Crypto products and NFTs are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions. All content provided is for informational purposes only, and shall not be relied upon as financial/investment advice. Opinions shared, if any, are only shared for information and education purposes. Although the best efforts have been made to ensure all information is accurate and up to date, occasionally unintended errors or misprints may occur. We recommend you to please do your own research or consult an expert before making any investment decision. You may write to us at [email protected].